ISA 220 Scope. ISA provides the level of abstraction between the software and the hardware One of the most important abstraction in CS Its narrow well-defined and mostly static compare writing a windows emulator almost impossible to writing an ISA emulator a few thousand lines of code.

2

Requirements within the ISAs have or have not been addressed within the ISA for LCE.

Describe the requirements of isa 240. Its a generic philosophy and can be defined in many ways. The summary follows the standard structure of ISA which starts from Introduction and follow by Objective Definition Requirement and finally Application of Standard. ISA 240103 Describe the national requirement in circumstances where the auditors ability to continue performing the audit is brought into question.

International Standard on Auditing ISA 240 The Auditors Responsibilities Relating to Fraud in an Audit of Financial Statements should be read in conjunction with ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. ASA 240 StandardsAccounting Auditing as amended taking into account amendments up to ASA 2011-1 - Amendments to Australian Auditing Standards - June 2011 These Auditing Standards establish requirements and provide applications and other explanatory material to auditors regarding their responsibilities relating to fraud in an audit of a financial report. ISA 240 The Auditors Responsibilities Relating to Fraud in an Audit of Financial Statements ISA 250 Consideration of Laws and Regulations in an Audit of Financial Statements ISA 260 Communication with Those Charged with Governance ISA 265 Communicating Deficiencies in Internal Control to Those Charged with Governance and Management.

The responsibility of auditor towards it and. For the category referred to in paragraph 6a the auditors responsibility is to obtain sufficient appropriate audit evidence regarding compliance with the provisions of those laws and regulations. Minimal requirements have been included for.

Alignment principles have been developed to help explain why an ISA requirement has been. International Standard on Auditing UK ISA UK 240 Revised 2021 The Auditors Responsibilities Relating to Fraud in an Audit of Financial Statements should be read in conjunction with ISA UK 200 Revised June 2016 Overall Objectives of the Independent. In complying with the requirements of ISA UK 240 Revised the auditor may also need to consider whether there has been non-compliance with laws and regulations and therefore that requirements in ISA UK 250 Sections A and B Revised November 2019 also apply.

Exhibit 1 sets out statements in ISA 240 that use the present tense to describe auditor actions and the proposed treatment of whether the actions should be redrafted as a requirement or redrafted to make clear that it is explanatory material. ISA 240 the Auditors Responsibilities Relating to Fraud in an Audit of Financial Statements recognises that misstatement in the financial statements can arise from either fraud or error. Intentional act of misrepresentation.

International Standard on Auditing ISA 240 The Auditors Responsibilities Relating to Fraud in an Audit of Financial Statements should be read in conjunction with ISA 200 Overall Objectives of the I ndependent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. Auditing Standard ASA 240 establishes mandatory requirements and provides explanatory guidance on the auditors responsibility to consider fraud in an audit of a financial report and expand on how the standards and guidance in ASA 315 Understanding the Entity and its Environment and Assessing the. It also addresses where applicable the responsibilities of the engagement quality control reviewer.

Acknowledging their management responsibility for the design implementation and maintenance of internal control to prevent and detect fraud that they have disclosed to the auditor managements. ISA 250 202 7. International Standard on Auditing Ireland ISA Ireland 240 Updated December 2018.

As described in ISA Ireland 200. The auditor should document the matters set out in paragraphs 107 to 110 of ISA 240. Describe the national requirements for documentation.

Paragra ph references to extant ISA 240. Consideration of Fraud in a Financial Statement Audit 165 Effective Date09 Thissectioniseffectiveforauditsoffinancialstatementsforperiods endingonorafterDecember152012. ISA 250 Consideration of Laws and Regulations in an Audit of Financial.

In this ISA differing requirements are specified for each of the above categories of laws and regulations. Responsibility for the prevention and detection of fraud auditor the external auditor must obtain written representations from management. The distinguishing factor is whether the underlying action that resulted in the misstatement was intentional or unintentional.

There is also a brief supporting description with regard to how the ISA for LCE aligns to the ISAs in the last column of the table. Audit evidence contradicting other evidence. This is the complete summary of ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing.

Requirements in this ISA Ireland are designed to assist the auditor in identifying and. ISA 220 deals with the specific responsibilities of the auditor regarding quality control procedures for an audit of financial statements. ISA 240 Redrafted further requires that.

This ISA is to be read in conjunction with relevant ethical requirements. But in concise manner we can define fraud as. The auditor is responsible for maintaining an attitude of professional skepticism throughout the audit ISA 240 Redrafted paragraph 8.

The Conduct of an Audit in Accordance with International Standards on Auditing Ireland paragraph A51. This was published when the requirements only applied to audits of public interest entities but it may be helpful to auditors of all entities where ISAs UK apply. Dealing with fraudulent activities if found.

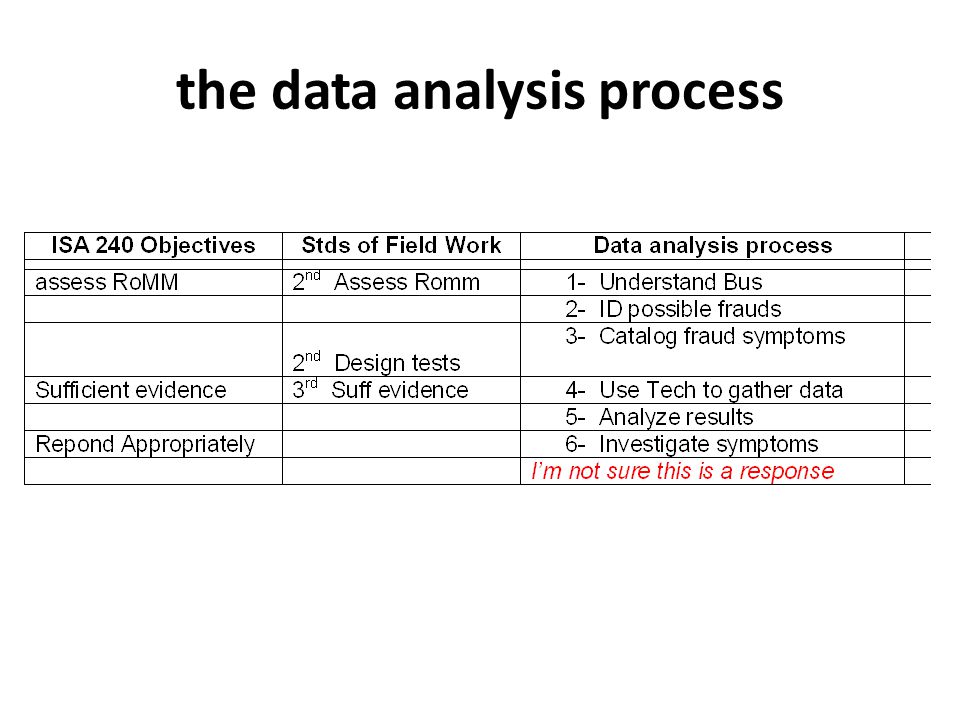

ISA UK 240 Revised June 2016 Updated January 2020 The Auditors Responsibilities Relating to Fraud in. ISA 240 lays down the requirements on. Analysis of ISA 240 and Mapping Document 1.

The requirements in the ISA column reflect the most recently approved ISAs some of which may not yet be effective including ISA 540 Revised ISA 315 Revised 2019 and ISA 220 Revised and any related conforming and consequential amendments to the ISAs. 2 What is Fraud in audit. ASA 240 StandardsAccounting Auditing as made.

Professional skepticism is of key importance to the audit for example requiring auditors to be alert to. Is it sufficiently clear in these ISAs UK of the interaction between them.

Chapter 6 Data Driven Fraud Detection Sampling Isa 240 Emphasizes That Fraud Is More Difficult To Detect Than Unintentional Errors Errors Sampling Is Ppt Download

Komentar